XRechnung – Quoting VAT on Used Parts

What has changed with electronic invoicing and how to solve problems regarding differential taxation

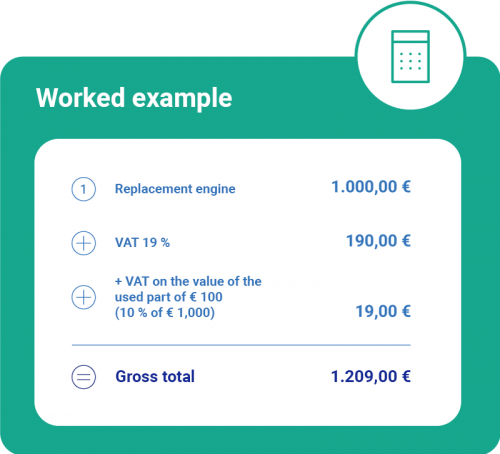

Example:

== Tax Calculation ==

The VAT on used parts equates to the full current VAT rate levied on an assessment basis, to be determined as per section 10 (2) sentence 2 UStG. The assessment basis is an average value defined as being 10% of the list price of the equivalent new component (exclusive of discounts and VAT).

Since the assessment basis for the used part is defined as being an average value of 10% of the list price of the equivalent new part, the VAT on the value of the old part has to be calculated in a separate invoice line (19% of €100). Up to this point, the process is in line with KoSIT recommendations. The problem now, however, is that the full net value has already been taxed and that you cannot repeat the taxation without falsifying the net total since you would have to increase it by the “fictive” assessment basis for the used part in a separate invoice line.

Numerous companies are currently facing these difficulties – after all, the VAT in question affects automotive businesses and manufacturers whose products are bound to need some parts replaced eventually.

If you too are struggling with this problem, please do not hesitate to contact us.